Retail as a Land Allocation Question

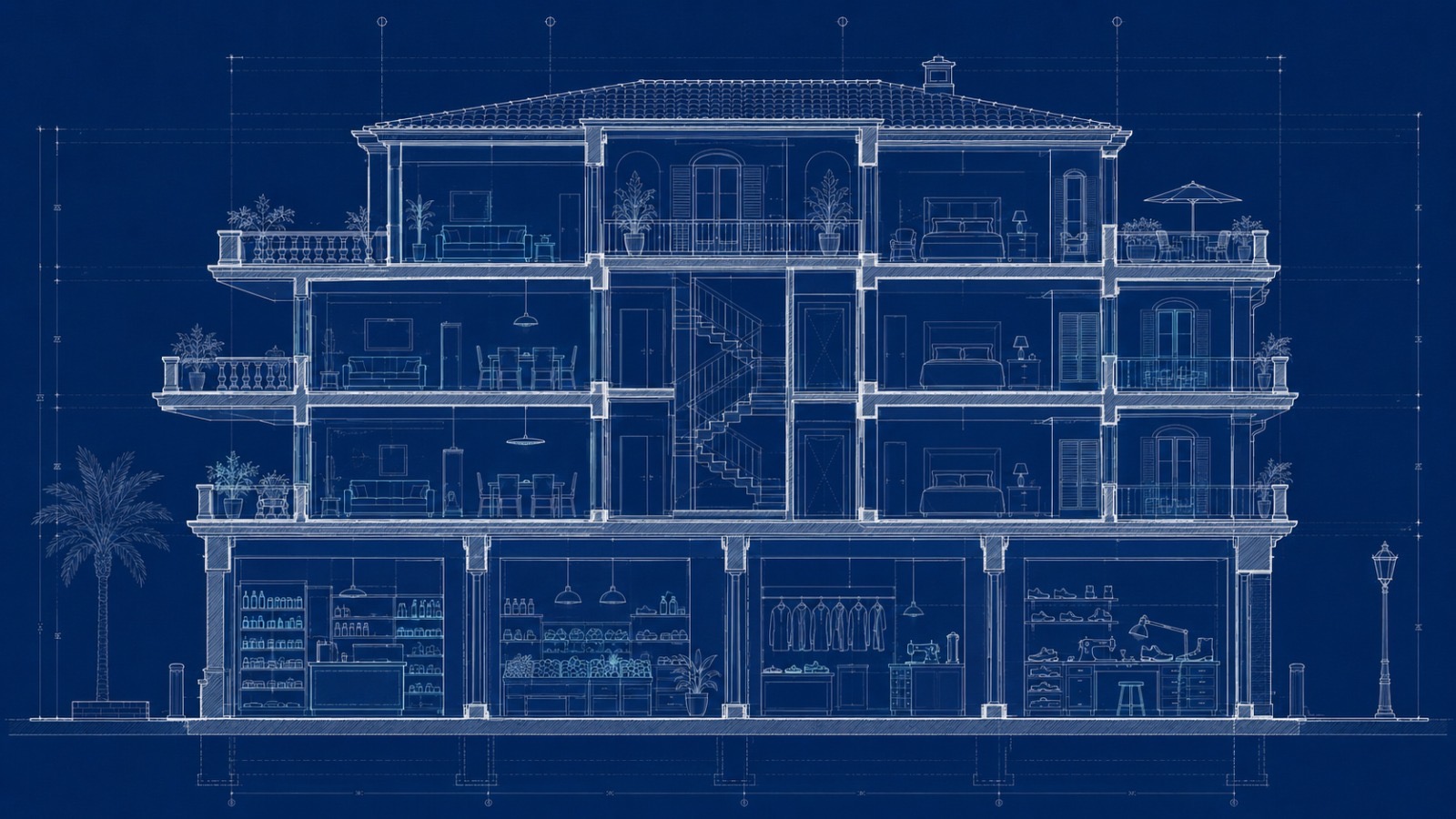

GuidelinesRetail occupies a unique position within Monaco's economy. While the Principality is often associated with luxury, its retail landscape also serves the daily needs of residents, cross-border commuters and regular visitors.

Recent data published by IMSEE illustrates an interesting paradox. Over the past decade, retail turnover has increased from approximately €900 million to more than €2.3 billion. The sector is clearly expanding. Yet this growth has not translated into a uniform strengthening of Monaco's retail fabric.

Much of the increase has been driven by high-value activities such as jewellery, luxury fashion, prestige automotive and specialist retailers serving an international clientele. By contrast, everyday retail and local services face increasing pressure.

The demographic profile of the sector reflects this evolution. Nearly one business in two has been established for less than ten years, illustrating both a capacity for renewal and the difficulty of sustaining certain business models in one of Europe's most expensive real estate markets.

A Rational Market Outcome

The underlying mechanism is straightforward.

In a market where commercial premises are overwhelmingly privately owned, retail space naturally gravitates towards occupiers capable of supporting the highest rental values. From the perspective of an individual landlord, this is entirely rational. It maximises the performance of the asset.

The conclusion becomes less obvious once the analysis shifts from the individual retail unit to the building or the district as a whole.

Not all retail activities generate the same rental potential.

Nor do they contribute equally to the quality of an address.

A pharmacy, dry cleaner, delicatessen, bookshop or alterations service may never support the same rents as a luxury retailer or a premium restaurant. Yet their presence may significantly influence the day-to-day functioning of a residential building and, ultimately, the attractiveness of the surrounding neighbourhood.

The question is therefore not whether luxury retail should replace neighbourhood retail.

It is whether the performance of a commercial unit should be assessed solely at the scale of the lease itself.

A Retail Geography in Transition

These dynamics are already visible across Monaco.

Monte-Carlo's Carré d'Or is naturally oriented towards international luxury retail. La Condamine remains the Principality's primary neighbourhood shopping district, while Fontvieille revolves around its retail centre.

Other areas are evolving differently. Districts such as Larvotto and Mareterra, despite their significant residential development, currently offer a more limited range of everyday services.

This does not necessarily represent an imbalance.

It reflects the fact that each district serves a different purpose.

The more interesting question is whether this distribution should remain entirely market-driven, particularly in newly developed neighbourhoods.

Rethinking the Commercial Dimension of a Development

When a residential development is conceived, virtually every component is carefully considered: architecture, materials, circulation, amenities and services.

The commercial element is often treated differently.

In most cases, the final retail offering emerges through market forces alone. That approach is economically coherent, but it does not always produce the combination of uses best suited to the long-term positioning of the building or the district.

Developers are naturally the first stakeholders able to address this question.

Long before the first lease is signed, they determine the identity of the project.

Once a building has been delivered, condominium regulations can extend that initial vision by defining permitted or prohibited activities. Used carefully, they can preserve the coherence of a development over time. Such restrictions are not without consequence, however, as they may reduce liquidity and affect the market value of commercial premises.

Public authorities retain a complementary role. Rather than intervening in individual buildings, they are uniquely positioned to assess commercial provision across the territory, identify underserved districts and guide future developments where appropriate.

Beyond Retail

Ultimately, this discussion extends well beyond retail itself.

It concerns how mixed-use developments are conceived in markets where land has become the scarcest resource.

Markets answer one question remarkably well: which occupiers can support prevailing rents?

They answer another far less naturally: which activities best support the long-term quality of a building or a neighbourhood?

As land becomes increasingly scarce, that second question is likely to become progressively more important.

Thinking about retail should not be viewed as an attempt to replace market forces.

Rather, it recognises that, in certain markets, the commercial dimension of a development deserves to be considered with the same attention as architecture, amenities and shared spaces.